Beranda

/ Deferred Tax Computation Format : Pdf Assessment Of Deferred Tax Recognition And Measurement Under Ifrs And Nigeria Sas An Empirical Examination : It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time.

Deferred Tax Computation Format : Pdf Assessment Of Deferred Tax Recognition And Measurement Under Ifrs And Nigeria Sas An Empirical Examination : It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time.

Insurance Gas/Electricity Loans Mortgage Attorney Lawyer Donate Conference Call Degree Credit Treatment Software Classes Recovery Trading Rehab Hosting Transfer Cord Blood Claim compensation mesothelioma mesothelioma attorney Houston car accident lawyer moreno valley can you sue a doctor for wrong diagnosis doctorate in security top online doctoral programs in business educational leadership doctoral programs online car accident doctor atlanta car accident doctor atlanta accident attorney rancho Cucamonga truck accident attorney san Antonio ONLINE BUSINESS DEGREE PROGRAMS ACCREDITED online accredited psychology degree masters degree in human resources online public administration masters degree online bitcoin merchant account bitcoin merchant services compare car insurance auto insurance troy mi seo explanation digital marketing degree floridaseo company fitness showrooms stamfordct how to work more efficiently seowordpress tips meaning of seo what is an seo what does an seo do what seo stands for best seotips google seo advice seo steps, The secure cloud-based platform for smart service delivery. Safelink is used by legal, professional and financial services to protect sensitive information, accelerate business processes and increase productivity. Use Safelink to collaborate securely with clients, colleagues and external parties. Safelink has a menu of workspace types with advanced features for dispute resolution, running deals and customised client portal creation. All data is encrypted (at rest and in transit and you retain your own encryption keys. Our titan security framework ensures your data is secure and you even have the option to choose your own data location from Channel Islands, London (UK), Dublin (EU), Australia.

Deferred Tax Computation Format : Pdf Assessment Of Deferred Tax Recognition And Measurement Under Ifrs And Nigeria Sas An Empirical Examination : It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time.. The former is based on the difference between accounting balance sheet and tax balance sheet while the later is. Deferred tax refers to income tax overpaid or owed due to the temporary differences between accounting income and taxable income. Calculating the beginning apic pool and the ongoing tax computations required by statement no. Accounting for deferred tax asset, deferred tax liability & permanent tax difference, reconcile pretax financial income with taxable income to determine. Deferred tax asset (dta) or deferred tax liability (dtl).

Deferred tax refers to income tax overpaid or owed due to the temporary differences between accounting income and taxable income. These taxes are eventually returned to the business in the form of tax relief. Assume tax rate of 20% and no temporary differences other than those stated above. However, deferred tax can also. Deferred tax asset (dta) or deferred tax liability (dtl).

Deferred Tax Asset Journal Entry How To Recognize from cdn.wallstreetmojo.com For example, read about different tax rates on short term / long term capital gain in india here: Its requirements can therefore be challenging, and the more. The former is based on the difference between accounting balance sheet and tax balance sheet while the later is. Deferred income tax and current income tax comprise total tax expense in the income statement. The term deferred tax expense refers to the income tax effect on a balance sheet arising out of difference taxable income calculated based it is the reason why the total tax expense reported in the income statement is usually not equal to the company's payable income tax according to the tax laws. National deferred tax row headings. Deferred taxes reconcile the tax basis of a balance sheet with the basis currently being used for valuing assets and recording liabilities. With respect to timing differences related to unabsorbed depreciation or carry forward losses, dta is recognised only if there is future virtual certainty.

Deferred tax assets originate when the amount of tax has either been paid or has been carried forward but it has still not been acknowledged in the statement of income.

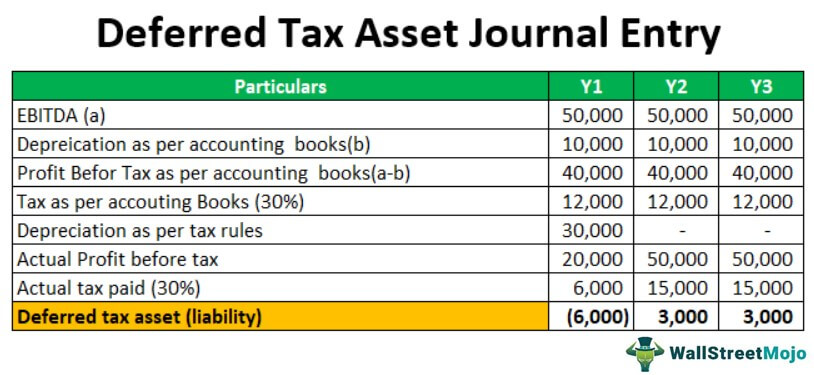

Taxable income for a deferred tax liability is income before tax less temporary differences. Computation of short term & long term capital gain tax in india. The deferred tax assets/liabilities to be recognised during different years would be computed as per the following table. Deferred tax expense results from changes in deferred tax assets and liabilities. For example, read about different tax rates on short term / long term capital gain in india here: So it will be a deferred tax asset (dta). Deferred tax liabilities are defined by this standard as the amounts of income taxes payable in future periods in respect of taxable temporary differences. Options and the deferred tax bite. The deferral also applies to deposits of the employer's share of social security tax that would otherwise be due after december 31, 2020, as long as the deposits relate to the tax imposed on wages paid (a) during the quarter ending on december 31, 2020, for employers filing quarterly employment. Calculate deferred tax as of 31 december year 1. Deferred tax assets originate when the amount of tax has either been paid or has been carried forward but it has still not been acknowledged in the statement of income. Introduction setting up deferred tax computation lead schedule and supporting working papers for temporary difference approach is inherently more complex that timing different approach. Deferred tax is the difference of income tax liability on profits derived as per books and profits derived as per income tax computation.

Deferred tax is a notional asset or liability to reflect corporate income taxation on a basis that is the same or more similar to recognition of profits than the taxation treatment. It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time. Last updated at may 29, 2018 by teachoo. Deferred tax liabilities can arise as a result of corporate taxation treatment of capital expenditure being more rapid than the. Creates deferred tax asset (dta).

Format Individual Tax Computation Students from imgv2-2-f.scribdassets.com However, deferred tax can also. In the given situation, excess tax paid today due to the difference among the income computed as per books of the company and the income. With respect to timing differences related to unabsorbed depreciation or carry forward losses, dta is recognised only if there is future virtual certainty. Deferred tax is the difference of income tax liability on profits derived as per books and profits derived as per income tax computation. Deferred tax expense results from changes in deferred tax assets and liabilities. The deferral also applies to deposits of the employer's share of social security tax that would otherwise be due after december 31, 2020, as long as the deposits relate to the tax imposed on wages paid (a) during the quarter ending on december 31, 2020, for employers filing quarterly employment. Assume tax rate of 20% and no temporary differences other than those stated above. Its requirements can therefore be challenging, and the more.

Deferred tax is a notional asset or liability to reflect corporate income taxation on a basis that is the same or more similar to recognition of profits than the taxation treatment.

The notion of temporary differences is fundamental to understanding deferred tax. On the package tab, select the deferred tax report, and verify that the deferred tax asset and deferred tax liability classifications based on your configuration are correct. Computation of short term & long term capital gain tax in india. Such a difference in tax primarily arises because of the timing difference when the tax is due and when the company pays it. 123(r) is a complex process requiring careful recordkeeping. Last updated at may 29, 2018 by teachoo. At the outset i think it is important to acknowledge that the accounting for deferred tax could have been a whole lot worse in the previous exposure drafts. Deferred tax is the difference of income tax liability on profits derived as per books and profits derived as per income tax computation. A deferred tax asset is an asset on a company's balance sheet that may be used to reduce its taxable income. The deferral also applies to deposits of the employer's share of social security tax that would otherwise be due after december 31, 2020, as long as the deposits relate to the tax imposed on wages paid (a) during the quarter ending on december 31, 2020, for employers filing quarterly employment. Deferred taxes reconcile the tax basis of a balance sheet with the basis currently being used for valuing assets and recording liabilities. Therefore, overpayment is considered an asset to the company. The term deferred tax expense refers to the income tax effect on a balance sheet arising out of difference taxable income calculated based it is the reason why the total tax expense reported in the income statement is usually not equal to the company's payable income tax according to the tax laws.

Deferred tax liabilities or deferred tax liability (dtl) is the deferment of the due tax liabilities. In year two, depreciation charged as per companies act and income tax act are same by which there is no deferred tax asset or liability. Last updated at may 29, 2018 by teachoo. These taxes are eventually returned to the business in the form of tax relief. On the package tab, select the deferred tax report, and verify that the deferred tax asset and deferred tax liability classifications based on your configuration are correct.

Ind As12 On Income Taxes from www.caclubindia.com A deferred tax asset is an asset on a company's balance sheet that may be used to reduce its taxable income. It is believed that the liabilities will be settled and the assets will be recovered eventually over time and at that point of time their tax consequences will. Both will appear as entries on a balance sheet and represent the negative and positive amounts of tax deferred tax typically refers to liabilities, wherein the amount entered on the balance sheet is payable at a future time. (b) deferred tax in respect of timing differences which reverse after the tax holiday period is recognised in the year in which the timing differences originate. The total amount by which the balance sheet value of current assets exceeds their taxable basis is calculated. Assume tax rate of 20% and no temporary differences other than those stated above. Deferred tax is a notional asset or liability to reflect corporate income taxation on a basis that is the same or more similar to recognition of profits than the taxation treatment. These taxes are eventually returned to the business in the form of tax relief.

Therefore, overpayment is considered an asset to the company.

Therefore, overpayment is considered an asset to the company. Deferred tax liabilities or deferred tax liability (dtl) is the deferment of the due tax liabilities. It is part of the accounting adjustment and gets eliminated as the temporary differences are reversed over time. National deferred tax row headings. The former is based on the difference between accounting balance sheet and tax balance sheet while the later is. Deferred tax liabilities, and deferred tax assets. The total amount by which the balance sheet value of current assets exceeds their taxable basis is calculated. Deferred tax assets originate when the amount of tax has either been paid or has been carried forward but it has still not been acknowledged in the statement of income. 123(r) is a complex process requiring careful recordkeeping. With respect to timing differences related to unabsorbed depreciation or carry forward losses, dta is recognised only if there is future virtual certainty. Learn more about deferred tax forms, deferred tax asset, deferred tax liability, dta and dtl calculation etc. On the package tab, select the deferred tax report, and verify that the deferred tax asset and deferred tax liability classifications based on your configuration are correct. Deferred tax refers to income tax overpaid or owed due to the temporary differences between accounting income and taxable income.